A Federal Grant Compliance Framework for Rural Organizations

Federal grants do not come with a single compliance deadline. They come with a compliance relationship that begins before the first dollar is drawn and does not end until the final report is accepted and the records retention clock starts running. For rural organizations managing federal awards with lean staff and limited administrative infrastructure, understanding what compliance requires at each stage of that relationship is the difference between a clean audit and a multi-year recovery effort.

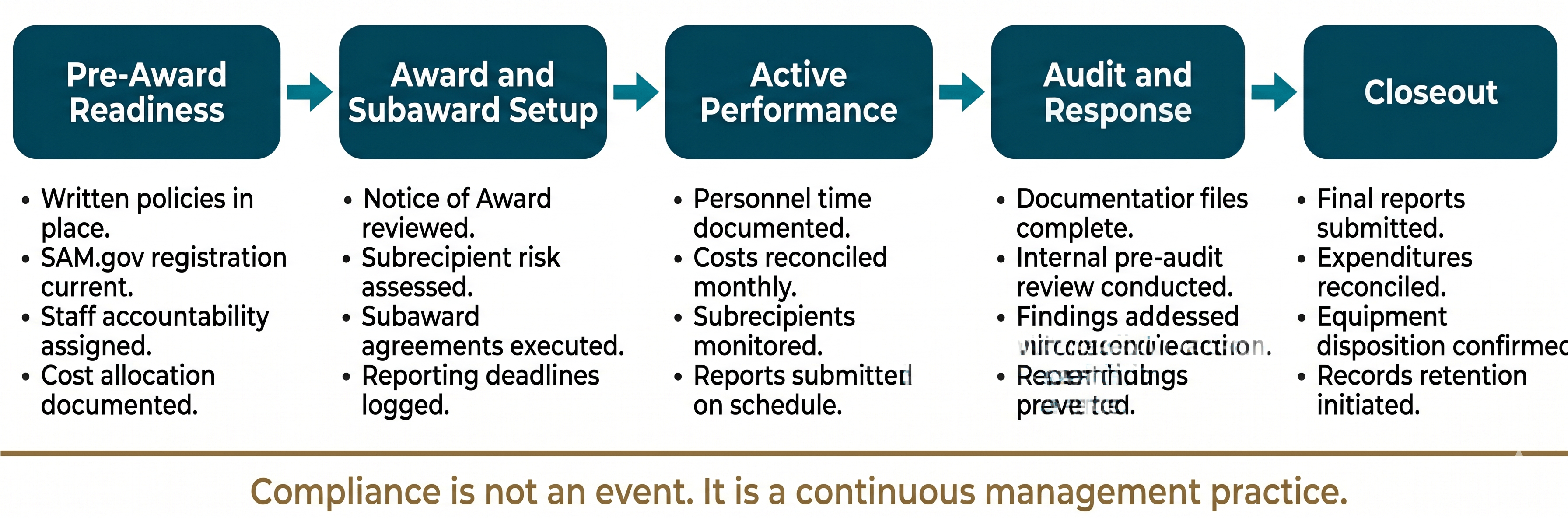

This framework organizes the core requirements of 2 CFR Part 200, the Uniform Guidance, along the grant lifecycle. Each stage introduces what is at stake, followed by the affirmative standards your organization should be meeting. No single page can substitute for the full regulatory text, but this framework gives you a working map of where compliance obligations arise, what they require, and what breaks down when they are not met.

For a plain-language walkthrough of the underlying regulatory requirements, visit the full 2 CFR Part 200 guide. Read a breakdown of the 2026 proposed updates to the Uniform Guidance.

Stage One: Pre-Award Readiness

What happens before you apply shapes everything that follows. Organizations that accept federal awards without the administrative systems to manage them do not develop those systems under the pressure of performance. They improvise, and improvisation under federal compliance requirements generates findings.

Pre-award readiness means your organization has the written policies, internal controls, and staff capacity in place to manage a federal award before the award arrives. It means your registrations are current, your cost allocation methodology is documented, and your procurement procedures reflect the current Uniform Guidance thresholds. Auditors do not give credit for infrastructure built after the fact.

Pre-award readiness is not a bureaucratic formality. It is the foundation on which each downstream compliance obligation rests.

Pre-Award Readiness Checklist

- Your organization maintains an active registration in SAM.gov with a current expiration date and accurate entity information.

- Your organization has a Unique Entity Identifier on file and is confirmed eligible to receive federal awards.

- Your organization has written procurement policies reflecting the current 2 CFR 200 thresholds, including the $15,000 micro-purchase threshold, the $350,000 simplified acquisition threshold, and the price reasonableness documentation requirement that applies at all spending levels.

- Your organization's procurement policies specify the most restrictive applicable standard, accounting for any state law or local charter requirements more stringent than the federal thresholds.

- Your organization has a written cost allocation methodology documenting how shared costs are distributed across programs and funding sources.

- Your organization has documented internal controls for federal grant expenditures, including written approval workflows, segregation of duties where staffing permits, and a reconciliation process between grant records and the general ledger.

- Your organization has identified staff with named responsibility for grant administration, including financial management, programmatic reporting, and subrecipient oversight where applicable.

- Your organization has reviewed the assistance listing for the program being pursued and understands the specific compliance requirements, matching obligations, and special tests and provisions applicable to that program.

- Your organization has assessed whether it meets all eligibility requirements for the program and has documentation supporting that determination.

Stage Two: Award Acceptance and Subaward Setup

When a federal award is accepted, a compliance clock starts. The terms and conditions in the Notice of Award are not suggestions. They are enforceable obligations, and failure to read them carefully before accepting is itself a compliance risk.

If your organization passes federal funds to another entity, a nonprofit partner, a contractor, or a local government subrecipient, your obligations under 2 CFR 200.332 begin at the moment of subaward execution, not at the moment an auditor asks for documentation. The federal government does not pursue the subrecipient for compliance failures. It pursues you.

Subaward setup is also the moment to verify that each vendor or partner your organization intends to work with is eligible to receive federal funds. A single unscreened vendor can generate a procurement finding regardless of how well the rest of the grant is managed.

Award Acceptance and Subaward Setup Checklist

- Your organization has reviewed the Notice of Award in full, including all terms, conditions, and special provisions, before accepting the award.

- Your organization has recorded the award period of performance, all reporting deadlines, and all required submission dates in a formal tracking system with named staff accountability for each item.

- Your organization has verified that all vendors and contractors to be engaged under the award have been screened against the federal System for Award Management suspension and debarment list prior to contract execution.

- Your organization has documented a formal risk assessment for each subrecipient receiving a pass-through of federal funds, evaluating the subrecipient's financial capacity, prior audit history, and experience managing federal awards.

- Your organization has executed written subaward agreements with each subrecipient that include all elements required under 2 CFR 200.332, including the federal award identification, applicable compliance requirements, reporting expectations, and audit requirements.

- Your organization has established a monitoring plan for each subrecipient specifying the frequency and method of financial and programmatic oversight throughout the performance period.

- Your organization has documented the equipment capitalization threshold applicable to this award, accounting for both the federal threshold of $10,000 and any more restrictive local or state threshold, and has communicated this threshold to relevant staff.

Stage Three: Active Performance and Ongoing Compliance

The performance period is where most compliance failures originate and where documentation discipline either protects your organization or exposes it. The findings that surface in Single Audits are rarely the result of fraud or deliberate noncompliance. They are the result of administrative systems that were not built to capture the evidence the Uniform Guidance requires.

Personnel costs are the single most common source of findings and appear across nearly each program type in the federal audit record. Semi-annual certifications for employees working solely on one federal program, personnel activity reports for employees splitting time across multiple programs, and supervisory approvals for all payroll charges to federal awards are not optional documentation practices. They are the evidentiary foundation for each salary dollar charged to a federal grant.

Cash management failures, procurement missteps, and reporting lapses also concentrate in this stage. Each represents a category of compliance obligation managed actively throughout the performance period, not reconstructed at audit time.

Active Performance Checklist

- Your organization charges only allowable, allocable, and reasonable costs to federal awards, consistent with 2 CFR Part 200 Subpart E and the specific requirements of the applicable assistance listing.

- Your organization maintains semi-annual certifications for each employee whose salary is charged entirely to a single federal program, signed by the employee or a responsible supervisor with firsthand knowledge of the work performed.

- Your organization maintains personnel activity reports for each employee whose salary is charged across multiple cost objectives, documenting the actual distribution of effort on a schedule sufficient to support the charges made.

- Your organization reviews and reconciles payroll charges to federal awards at least monthly, confirming charges align with the documented effort distribution and the approved budget.

- Your organization processes all reimbursement requests based on actual expenditures incurred, not projected or anticipated costs, and retains documentation supporting each draw.

- Your organization minimizes the time between advance draws of federal funds and actual disbursement, consistent with the cash management requirements of 2 CFR 200.305, and does not retain federal funds in interest-bearing accounts beyond the permitted threshold.

- Your organization uses procurement methods appropriate to the dollar value and complexity of each purchase, documents competitive solicitation or price reasonableness for all purchases regardless of amount, and retains procurement records including solicitation documents, responses received, and the basis for vendor selection.

- Your organization conducts and documents monitoring reviews of each subrecipient on the schedule established at subaward, including review of financial reports, programmatic progress, and any audit findings applicable to the subrecipient.

- Your organization takes timely corrective action when subrecipient monitoring identifies compliance concerns, and documents both the concern identified and the corrective action taken.

- Your organization submits all required performance reports, financial reports, and federal financial reports on the schedule specified in the Notice of Award and retains copies of all submissions.

- Your organization tracks grant reporting deadlines in a formal system separate from general calendar reminders, with named staff accountability and advance notification for each required submission.

- Your organization maintains a physical inventory of equipment purchased with federal funds and conducts required physical inventories on the schedule specified in 2 CFR 200.313.

- Your organization tracks items with a per-unit acquisition cost between $5,000 and $9,999 in a sensitive items inventory even where those items are federally classified as supplies under the 2024 threshold revision, consistent with your local fiduciary obligations.

Stage Four: Audit Preparation and Response

For organizations expending $1,000,000 or more in federal awards in a fiscal year, a Single Audit is required. For organizations below that threshold, program-specific audits or desk reviews may still occur. In either case, audit readiness is not a condition you achieve in the weeks before the auditor arrives. It is the condition your documentation systems either maintain continuously or fail to produce on demand.

The audit record shows clearly that organizations with formal written policies, complete contemporaneous documentation, and active internal controls resolve findings quickly when findings occur. Organizations without those systems spend months or years reconstructing records, responding to repeat findings, and managing the budget uncertainty accompanying unresolved questioned costs.

Audit preparation is also the stage where your organization's corrective action discipline is tested. A finding acknowledged and not corrected becomes a repeat finding. A repeat finding signals systemic failure to federal program officers and invites escalating scrutiny.

Audit Preparation and Response Checklist

- Your organization maintains a complete documentation file for each federal award, organized to support audit review, including the Notice of Award, approved budget, all amendments, financial reports, performance reports, procurement records, personnel documentation, and subrecipient monitoring records.

- Your organization retains all federal award records for the period required under 2 CFR 200.334, which is three years from the date of submission of the final expenditure report, or longer where program-specific requirements apply.

- Your organization conducts an internal pre-audit review of grant documentation at least annually, identifying gaps in documentation before an external auditor does.

- Your organization responds to audit findings within the timeframes specified by the cognizant agency or oversight body, and submits corrective action plans that include named responsible parties, specific remediation steps, and realistic completion dates.

- Your organization implements corrective actions from prior audit findings fully and verifiably, and monitors implementation through the subsequent audit cycle to prevent repeat findings.

- Your organization tracks the status of all open audit findings across federal programs in a single log maintained by named staff, with documented progress toward resolution.

Stage Five: Closeout

Closeout is the stage most often treated as a formality and the stage most likely to generate findings when treated that way. Federal award closeout requires your organization to reconcile all expenditures, return any unobligated federal funds, submit final reports, and confirm the disposition of equipment and supplies purchased with federal funds. Failure to complete any of these steps on time can result in questioned costs, disallowed expenditures, or audit findings in the subsequent program year.

The 2024 Uniform Guidance revisions adjusted the residual supplies threshold at closeout from $5,000 to $10,000. Your organization may now retain a larger dollar value of unused supplies post-grant without compensation to the federal awarding agency. However, taking advantage of that flexibility requires your organization to have tracked supplies accurately throughout the performance period and to have updated its internal policies to reflect the revised threshold.

Closeout Checklist

- Your organization submits all final reports, including the final federal financial report and final performance report, within the timeframe specified in the Notice of Award or applicable program regulations.

- Your organization reconciles all final expenditures to the general ledger and to the approved grant budget before submitting the final financial report, and retains documentation supporting the reconciliation.

- Your organization returns any unobligated federal funds remaining at the end of the period of performance within the required timeframe.

- Your organization conducts a final inventory of equipment purchased with federal funds and determines the appropriate disposition method consistent with 2 CFR 200.313, including whether federal agency approval is required for transfer or sale.

- Your organization calculates the residual value of unused supplies at grant closeout and determines whether compensation to the federal awarding agency is required under the applicable threshold.

- Your organization confirms that all subrecipient obligations have been closed, final subrecipient reports have been received and reviewed, and any subrecipient audit findings have been resolved or are actively being addressed.

- Your organization initiates the records retention period from the date of submission of the final expenditure report and communicates the retention end date to relevant staff.

The Compliance Ecosystem Behind the Lifecycle

The lifecycle frame above gives you a stage-by-stage map of when compliance obligations arise. But compliance failures rarely respect stage boundaries. A procurement weakness in Stage One produces a finding in Stage Three or Stage Four. A subrecipient monitoring gap established in Stage Two surfaces as questioned costs in Stage Five. Documentation discipline applied inconsistently during Stage Three creates an impossible reconstruction task in Stage Four.

The practical implication is that compliance is not a checklist completed once per stage. It is a set of ongoing management practices that compound across the life of an award. Organizations that build the systems once and maintain them consistently are the organizations whose audits close cleanly. Organizations that address compliance reactively, responding to findings after they occur rather than preventing them through continuous documentation, spend disproportionate staff time and organizational resources managing consequences.

Rural organizations face a specific version of this challenge. Staff turnover disrupts institutional knowledge of grant requirements. Small office sizes limit the segregation of duties the Uniform Guidance assumes. Limited professional development budgets mean compliance training often falls behind regulatory changes. The 2024 Uniform Guidance revisions and the proposed 2026 updates represent exactly the kind of regulatory change creating compliance exposure for organizations operating on prior-cycle knowledge.

The framework on this page reflects the requirements in effect as of the 2024 Uniform Guidance revisions. Read about the proposed 2026 updates.

Is Your Organization Audit-Ready?

Knowing the standards is the starting point. Knowing where your organization stands against them is what drives action.

The Rural Capacity Session is a structured working conversation covering your organization's federal grant compliance posture across the areas generating the most audit exposure in the current Single Audit cycle. It produces a clear picture of where your systems are sound, where gaps exist, and what your organization should address before your next award or your next audit.